Global markets volatile as fears of Russia disrupting energy supplies caused energy prices to spike. Spiralling living costs on higher inflation, looming rate rises, borrowing costs, led equity markets to seesaw.

GLOBAL MARKETS

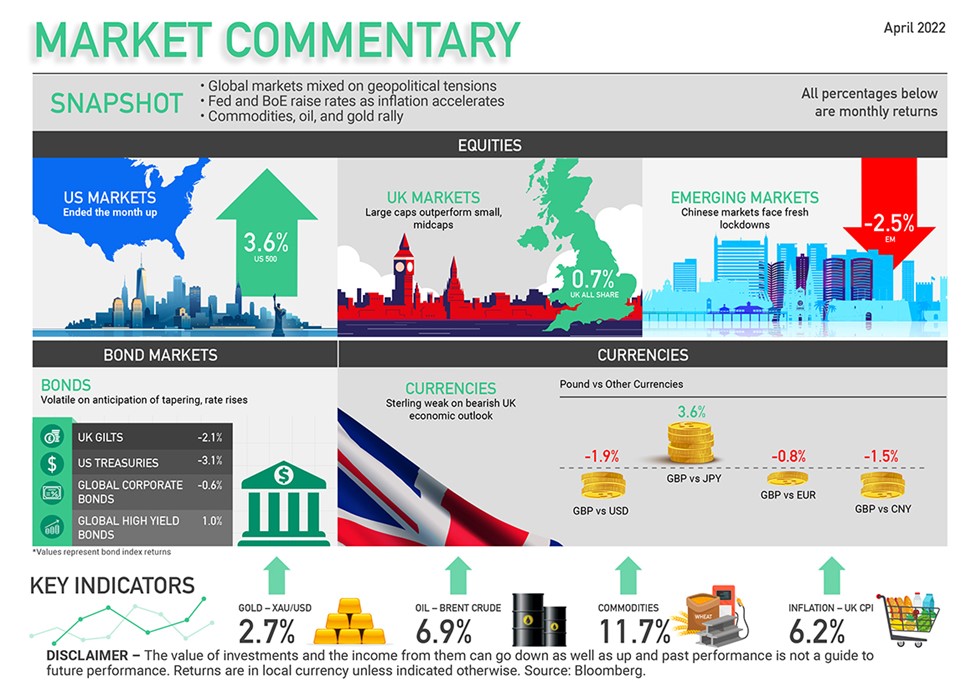

US MARKETS

Equity markets swung often during the month

US equity markets ended the month stronger despite some sharp moves in both bonds and equities intra month. Bond and equity markets swung between risk on and risk off, with investors navigating between speculative trading (tech stock rally) and preserving capital (defensive large cap equities). US annual inflation reached 7.9% in March. Fed began quantitative tightening, raising rates for the first time since 2018, but by a modest 0.25%. Monetary tightening is expected to gather pace as the bank looks to reduce its $9trn balance sheet. Up 3.6% (US 500)

EUROPEAN MARKETS

The war in Ukraine heavily impacting the region

Eurozone shares remained subdued as the close proximity to the war in Ukraine, as well as the region’s reliance on Russian energy, caused supply worries and fuelled energy price spikes. The ECB, previously dovish on rates, changed their rhetoric as annual inflation in the area rose to 7.5% from 5.9% in February. Any chance of a ceasefire in the region, with Russia and Ukraine entering negotiations in Turkey, may allow the Eurozone to regain some semblance of stability. Up 0.6% (Euro 600 Index)

UK MARKETS

Inflation and Spring statement weigh on the markets

UK markets rose modestly over the month as the Chancellor’s Spring statement weighed on investor sentiments. UK CPI inflation reached a 30-year high of 6.2%, translating into a hefty fall in disposable incomes alongside rising NI contributions. Large cap stocks, as tracked by FTSE 100, outperformed small and midcaps due to its large weighting in oil & gas and mining stocks. Meanwhile, in an effort to tackle inflation, BoE raised rates for the third time by 0.25% to 0.75%. Up 0.7% (UK All Share)

ASIAN MARKETS

Lockdowns in China a cause for concern

Japanese stock market was strong as BoJ Governor Kuroda vowed to maintain ultra-loose monetary policy in stark contrast to Western developed markets. The bank’s target range of +/-0.25% is being maintained. Emerging Market equities fell as geopolitical tensions, inflation and deteriorating growth outlook impacted the region adversely. China lagged overall EM, as lockdowns were imposed in several cities to curb rising Omicron COVID-19 cases. Shanghai suspended manufacturing, public transport, and the financial hub, effectively shutting down production. Down 2.0% (Asia Index)

Need to know more? If you have a question, would like more information, or are seeking financial planning or Wealth Management advice please contact hello@jarrovian.co.uk

DISCLAIMER – The value of investments and the income from them can go down as well as up and past performance is not a guide to future performance.

Jennifer Turner